Attorney-Approved Maine Promissory Note Template

Attorney-Approved Maine Promissory Note Template

In the beautiful state of Maine, individuals and businesses often turn to a Promissory Note form when a loan is made. This document plays a crucial role in setting the terms of the loan, ensuring clarity and commitment for both the lender and the borrower. It outlines the amount borrowed, the interest rate, repayment schedule, and what happens in the event of default. The versatility and enforceability of this document make it a fundamental tool in financial transactions, whether for personal loans, business start-ups, or other investments. Such a form not only provides legal protection but also promotes trust and reliability between the parties involved, making it a centerpiece in the financial landscape of Maine.

Maine Promissory Note Template

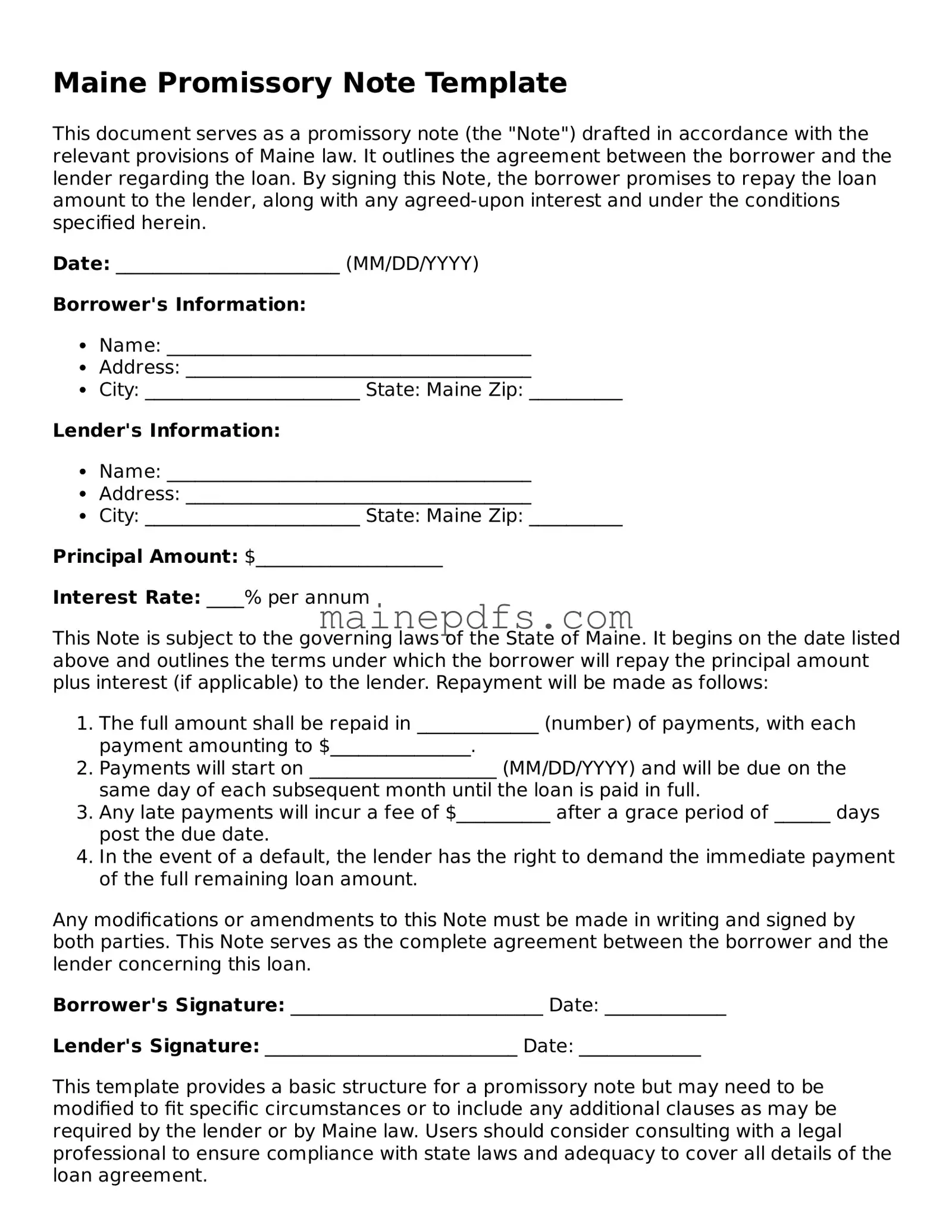

This document serves as a promissory note (the "Note") drafted in accordance with the relevant provisions of Maine law. It outlines the agreement between the borrower and the lender regarding the loan. By signing this Note, the borrower promises to repay the loan amount to the lender, along with any agreed-upon interest and under the conditions specified herein.

Date: ________________________ (MM/DD/YYYY)

Borrower's Information:

Lender's Information:

Principal Amount: $____________________

Interest Rate: ____% per annum

This Note is subject to the governing laws of the State of Maine. It begins on the date listed above and outlines the terms under which the borrower will repay the principal amount plus interest (if applicable) to the lender. Repayment will be made as follows:

Any modifications or amendments to this Note must be made in writing and signed by both parties. This Note serves as the complete agreement between the borrower and the lender concerning this loan.

Borrower's Signature: ___________________________ Date: _____________

Lender's Signature: ___________________________ Date: _____________

This template provides a basic structure for a promissory note but may need to be modified to fit specific circumstances or to include any additional clauses as may be required by the lender or by Maine law. Users should consider consulting with a legal professional to ensure compliance with state laws and adequacy to cover all details of the loan agreement.

| Fact | Detail |

|---|---|

| Definition | A Maine Promissory Note is a legal agreement in which one party promises to pay a certain amount of money to another party under specific terms. |

| Governing Law | Maine's promissory notes are governed by both state law and federal regulations, including the Uniform Commercial Code as adopted in Maine. |

| Types | There are two main types: secured and unsecured. A secured note includes collateral, while an unsecured note does not. |

| Interest Rate | The legal maximum interest rate is set by state law, and if not specified, the default interest rate applies as per the state's legal guidelines. |

| Requirements | It must include the amount borrowed, interest rate, repayment schedule, and signatures of both the borrower and the lender. |

| Usury Rate | If a promissory note's interest rate exceeds the legal limit, it could be considered usurious and subject to penalties or voiding. |

| Enforcement | In case of default, the lender may take legal action to enforce repayment, including taking possession of collateral for secured notes. |

| Signatures | Both the borrower and the lender must sign the note for it to be legally binding. Witnesses or notarization may be required for additional legal standing. |

| Prepayment | Borrowers might have the option to pay the note off early without penalty, depending on the terms of the agreement. |

| Template Use | Utilizing a state-specific template helps ensure that all legal requirements are met and the note is enforceable in Maine. |

Preparing a Maine Promissory Note is an important step for both lender and borrower in documenting a loan agreement. This document outlines the payment terms, interest rate, payment schedule, and the consequences of non-payment, creating a legally binding obligation for repayment. Ensuring all sections are filled out correctly helps to protect the interests of both parties and provides clarity on the loan's terms. Below are the step-by-step instructions to accurately complete the Maine Promissory Note form.

Once the Maine Promissory Note is fully completed and signed, it's important for both the lender and borrower to keep copies of the document. This ensures that both parties have access to the agreed terms and can refer to the document if any questions or disagreements arise. Proper documentation and adherence to the steps above will facilitate a smooth lending process and help maintain a positive relationship between the lender and borrower.

A Maine Promissory Note is a written promise to pay a certain amount of money to another party under specific terms. This legal document outlines the amount of money borrowed, the interest rate, repayment schedule, and the consequences if the borrower fails to repay the amount. In Maine, as in other states, promissory notes can be used for personal loans, business loans, or real estate transactions.

Yes, in Maine, there are primarily two types of promissory notes:

The interest rate for a Maine Promissory Note is agreed upon by the parties involved. However, it must comply with Maine’s usury laws to be legally enforceable. As interest rates can fluctuate based on the market and the nature of the agreement, parties are encouraged to verify the current legal limits to ensure compliance.

A properly structured Maine Promissory Note should include:

While Maine law does not require a promissory note to be witnessed or notarized to be legally binding, having a notary or witness can add a layer of protection against disputes. It helps verify the authenticity of the document and the identity of the signatories.

Yes, a Maine Promissory Note can be modified if both the lender and the borrower agree to the changes. The modifications should be made in writing, and both parties should sign the document detailing the changes to ensure that there is a clear record of the agreement.

If the borrower fails to repay the loan according to the terms of the Maine Promissory Note, several outcomes are possible:

Maine does not require promissory notes to be registered or recorded. However, maintaining an accurately signed and dated copy is crucial for both parties for record-keeping and enforcement purposes.

When filling out the Maine Promissory Note form, individuals often encounter several common pitfalls that can lead to misunderstandings or legal issues down the line. Being aware of these mistakes can help ensure the document is filled out correctly and protects the interests of all parties involved.

Not specifying the type of interest rate. The document should clearly indicate whether the interest rate is fixed or variable. Overlooking this detail can create confusion over payment amounts as the balance comes due.

Omitting the payment schedule. A detailed payment schedule should be included, outlining when payments are due and in what amounts. Failure to include this schedule can lead to disagreements over the timing and size of payments.

Inaccurate or missing information. Every section of the form should be filled out accurately. Misspellings, incorrect dates, or missing details can invalidate the agreement or cause issues in enforcement.

Not defining the terms for late payments. The note should clearly state the consequences of late payments, including any additional fees or interest rates applied. Without this, enforcing penalties for late payments becomes challenging.

Forgetting to specify the collateral. If the note is secured, the collateral being used should be clearly described. Neglecting to include this information can complicate matters if the borrower defaults.

Failure to include all parties' information. The note should list the legal names and addresses of all parties involved. Incomplete information can lead to difficulties in holding all parties accountable.

Not getting the form notarized. While not always required, having a promissory note notarized can add a level of legal protection. Overlooking this step may affect the document's enforceability in court.

Addressing these mistakes before finalizing the promissory note can significantly reduce the risk of future disputes. Both the borrower and the lender should carefully review the document to ensure completeness and accuracy, seeking legal advice if necessary.

When involved in financial transactions in Maine, particularly those that require a Promissory Note, there are several other forms and documents you might need to consider. These additional documents can provide further legal protection, clarify the terms of the transaction, and ensure compliance with state laws. Below is a list of up to 10 documents that are often used alongside the Maine Promissory Note form, each with a brief description of its purpose and relevance.

Understanding and preparing these documents, when applicable, ensures that all parties are well-informed and agree to the terms of the financial transaction. It is always advisable to consult with legal professionals when dealing with complex financial agreements to ensure compliance and protect one's interests. This holistic approach to managing your financial documents can significantly reduce the risk associated with lending or borrowing funds.

The Maine Promissory Note form shares similarities with an IOU (I Owe You) document. Both serve as written promises to pay a specific sum of money to another person or entity. The primary difference lies in the detail and formalities included; promissory notes often outline repayment terms, interest rates, and the consequences of non-payment in much more detail than an IOU, which might be a more informal agreement without specifying the repayment schedule or interest rates.

Another document similar to the Maine Promissory Note form is the Loan Agreement. Both documents are used to detail the terms under which money has been lent and must be repaid. However, a loan agreement is typically more comprehensive, often incorporating clauses related to the governance of the loan, amendments to the agreement, and detailed legal remedies in case of default. While a promissory note might be used for simpler transactions, loan agreements are more common in complex or significant financial undertakings.

A Mortgage Agreement is also akin to the Maine Promissory Note in that both involve the borrowing of money and the promise to repay. The critical difference is that a mortgage agreement specifically involves property as collateral. If the borrower fails to fulfill the repayment terms, the lender has the right to take possession of the property. While a promissory note can be secured or unsecured, a mortgage is inherently a secured debt, with the security interest being in real property.

The Bill of Exchange is another financial document similar to promissory notes but with a significant distinction. While a promissory note is a promise made by the borrower to pay back the lender, a bill of exchange involves three parties: the drawer, the drawee, and the payee. It is an order made by the drawer demanding the drawee to pay a certain amount to the payee. This instrument is widely used in international trade, contrasting with the more singular focus of a promissory note on the agreement between borrower and lender.

Lastly, the Line of Credit Agreement shares similarities with the Maine Promissory Note, both providing for the extension of credit from one party to another. However, a line of credit agreement typically offers a maximum credit limit that the borrower can draw on, repay, and redraw from during the life of the agreement, providing more flexibility than a promissory note, which usually details a loan of a fixed amount to be repaid over a set period. Whereas promissory notes are often utilized for single, defined transactions, lines of credit are designed to accommodate ongoing financial needs.

When it comes to filling out a Maine Promissory Note form, ensuring accuracy and clarity is not just beneficial—it's imperative. This legal document serves as a promise to pay back a loan, and its creation must be approached with a level of seriousness and attention to detail. Below is a list of dos and don'ts that can serve as a guide to avoid common pitfalls and ensure the process is handled appropriately.

Things You Should Do:

Things You Shouldn't Do:

Adhering to these guidelines when filling out a Maine Promissory Note will help ensure that the document is legally sound and reflects the agreement between the lender and the borrower accurately. Remember, a well-crafted promissory note not only provides a legal framework for the loan but also helps maintain positive relations between the parties involved by clearly laying out expectations and responsibilities.

When discussing the Maine Promissory Note form, several misconceptions frequently arise. These misunderstandings can complicate financial transactions and can affect both the lender and the borrower's rights and obligations. Here, we address the five most common misconceptions to clarify how promissory notes function in Maine.

A promissory note is the same as a loan agreement. While both documents are used in lending processes, they serve different purposes. A promissory note is a promise to pay a specific sum of money on demand or at a fixed or determinable future time. A loan agreement, however, outlines the detailed terms and conditions of the loan, including the repayment schedule, interest rate, and the obligations and rights of both parties. In short, a promissory note is a straightforward document that evidences a debt, whereas a loan agreement provides a comprehensive framework of the loan's terms.

Promissory notes are informal and do not require legal formalities. This is not accurate. In Maine, as in other jurisdictions, certain legal formalities must be followed for a promissory note to be enforceable. For instance, the note must be in writing, signed by the borrower, and must clearly state the amount to be paid, the interest rate if any, and the repayment terms. Ignoring these requirements can result in a promissory note being considered invalid or unenforceable in a court of law.

All promissory notes are the same. There are actually several types of promissory notes, including secured and unsecured notes. A secured promissory note is backed by collateral that the lender can seize if the borrower fails to repay the loan. An unsecured promissory note does not involve collateral, making it riskier for the lender. The terms and conditions will vary depending on the nature of the promissory note and the agreement between the parties involved.

You don't need an attorney to create a valid promissory note in Maine. While it's true that you can draft a promissory note without legal assistance, consulting with an attorney can ensure that the document complies with Maine laws and adequately protects your interests. An attorney can also advise on the implications of the note's terms and whether it needs to be secured by collateral. Given the potential complexities and legal requirements, seeking professional advice is wise to avoid unintended consequences.

Once signed, the terms of a promissory note cannot be changed. Actually, the terms of a promissory note can be modified, but any alterations must be agreed upon by all parties involved. Both the borrower and the lender must consent to any changes in the note's conditions, and the amendments should be documented in writing to avoid future disputes. A modified agreement, sometimes called a modification agreement or an amendment, should be attached to the original promissory note to ensure clarity and legal enforcement.

Understanding these points about promissory notes in Maine can help both lenders and borrowers navigate their financial transactions more effectively, ensuring that their rights are protected and that they are complying with the legal framework.

When dealing with the Maine Promissory Note form, it's important to understand its purpose and how to properly fill it out. Below are key takeaways that can guide individuals through this process:

By keeping these key points in mind, individuals can ensure that their Maine Promissory Note is completed properly and that they understand the obligations it creates.

Maine Firearm Bill of Sale - The form can be used in various jurisdictions, helping to comply with local and state laws concerning private firearm sales.

How to Make a Purchase Agreement - A foundational document in any property transaction that outlines the terms of the sale and purchase agreement.

Operating Agreement Llc Maine - It helps establish clearer relationships with banks and investors by detailing the company's management and operational structure.