Download Maine Tax Template in PDF

Download Maine Tax Template in PDF

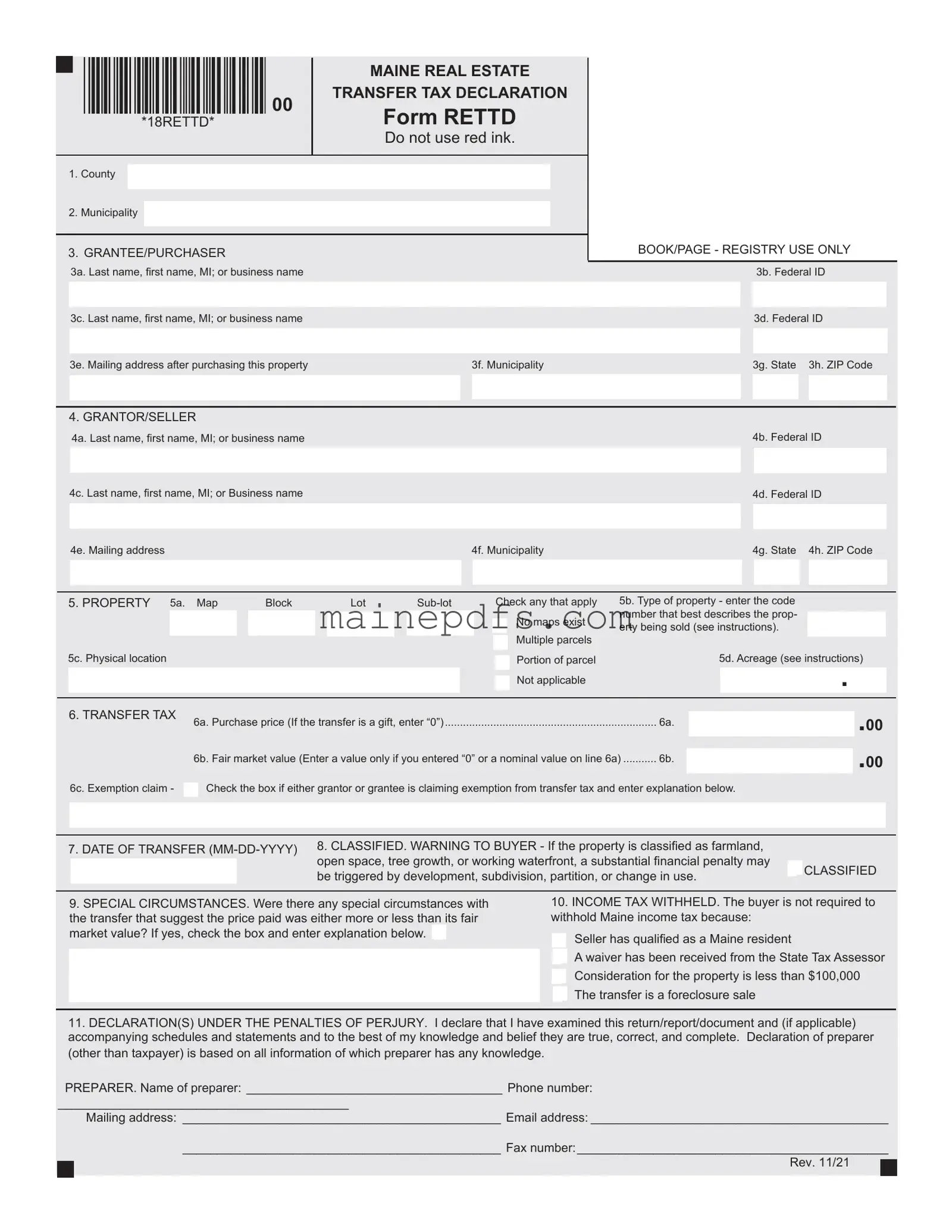

Engaging with the Maine Real Estate Transfer Tax Declaration Form RETTD unfolds a labyrinth of legislative requirements and tax implications for both buyers and sellers within the picturesque state of Maine. At its core, the form facilitates the legal transfer of property by capturing details ranging from the identification of the involved parties, marked by names and federal ID numbers, to the intricate descriptions of the property being transferred. It's a choreography of logistics, where participants must navigate through stipulated fields such as counties, municipalities, and the very nature of the property itself – whether it's a verdant farm or a commercial hub. The declaration is foundational in calculating the transfer tax, a cost shared equally between the seller and buyer, based on the property's sale price or fair market value, wherein lies the art of discerning the true worth of land and bricks. Stipulations for exemptions, the ominous warnings for properties classified under beneficial land-use categories, and the dire implications for noncompliance weave through the document, echoing Maine's commitment to maintaining its environmental and cultural heritage. This form—updated in November 2021—stands not just as a procedural necessity but as a reflection of Maine's legal landscape, bearing implications for residential dreams and commercial ventures alike, all under the watchful eyes of the state's legal framework and market conditions.

|

|

|

MAINE REAL ESTATE |

|

|

|

|

|

|

00 |

TRANSFER TAX DECLARATION |

|

|

Form RETTD |

|

|

*18RETTD* |

|

|

|

|

|

|

|

|

|

Do not use red ink. |

|

|

|

|

1.County

2.Municipality

3.GRANTEE/PURCHASER

3a. Last name, fi rst name, MI; or business name

3c. Last name, fi rst name, MI; or business name

3e. Mailing address after purchasing this property |

3f. Municipality |

|

|

|

|

BOOK/PAGE - REGISTRY USE ONLY

3b. Federal ID

3d. Federal ID

3g. State 3h. ZIP Code

4. GRANTOR/SELLER

|

4a. Last name, fi rst name, MI; or business name |

|

|

4b. |

Federal ID |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4c. Last name, fi rst name, MI; or Business name |

|

|

|

|

|

|

|

|

|

|

|

4d. |

Federal ID |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4e. Mailing address |

4f. Municipality |

4g. |

State 4h. ZIP Code |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. PROPERTY 5a. Map |

|

Block |

|

Lot |

|

Check any that apply |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

No maps exist |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Multiple parcels |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

5c. Physical location |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Portion of parcel |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Not applicable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5b. Type of property - enter the code number that best describes the prop- erty being sold (see instructions).

5d. Acreage (see instructions)

.

6. TRANSFER TAX |

6a. |

Purchase price (If the transfer is a gift, enter “0”) |

6a. |

|

|

.00 |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

||

|

6b. |

Fair market value (Enter a value only if you entered “0” or a nominal value on line 6a) |

6b. |

|

|

||

|

|

|

|

|

|

|

|

6c. Exemption claim -  Check the box if either grantor or grantee is claiming exemption from transfer tax and enter explanation below.

Check the box if either grantor or grantee is claiming exemption from transfer tax and enter explanation below.

7. DATE OF TRANSFER |

8. CLASSIFIED. WARNING TO BUYER - If the property is classifi ed as farmland, |

|

|

||

open space, tree growth, or working waterfront, a substantial fi nancial penalty may |

|

|

|||

|

|

|

|

CLASSIFIED |

|

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

be triggered by development, subdivision, partition, or change in use. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9.SPECIAL CIRCUMSTANCES. Were there any special circumstances with

the transfer that suggest the price paid was either more or less than its fair market value? If yes, check the box and enter explanation below.

10.INCOME TAX WITHHELD. The buyer is not required to withhold Maine income tax because:

Seller has qualified as a Maine resident

Seller has qualified as a Maine resident

A waiver has been received from the State Tax Assessor

A waiver has been received from the State Tax Assessor

Consideration for the property is less than $100,000

Consideration for the property is less than $100,000  The transfer is a foreclosure sale

The transfer is a foreclosure sale

11.DECLARATION(S) UNDER THE PENALTIES OF PERJURY. I declare that I have examined this return/report/document and (if applicable) accompanying schedules and statements and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

PREPARER. Name of preparer: _____________________________________ Phone number:

__________________________________________

Mailing address: ______________________________________________ Email address: ___________________________________________

______________________________________________ Fax number:_____________________________________________

Rev. 11/21

Real Estate Transfer Tax Declaration

Instructions

The Real Estate Transfer Tax Declaration (Form RETTD) must be fi led with the county Registry of Deeds when the accompanying deed is recorded. The Registry of Deeds will collect a tax based on the value of the transferred property. The tax is equals $2.20 for each $500 of value and is imposed half on the purchaser and half on the seller. If the transferred property is in more than one municipality or if there are more than two sellers or buyers, a Supplemental Form must be completed. For more information, visit www.maine.gov/ revenue/propertytax/transfertax/transfertax.htm or contact the Property Tax Division at

Line 1. County. Enter the name of the county where the property is lo- cated. If the property is in more than one county, complete separate Forms

RETTD.

Line 2. Municipality. Enter the name of the municipality where the prop- erty is located. If the transferred property is located in more than one mu- nicipality, complete a Supplemental Form.

Line 3. Grantee/Purchaser. a) & c): Enter one name on each available line, beginning with last name fi rst. If more than two purchasers, complete a Supplemental Form. b) & d): If a business entity is entered on a) or c), enter the entity’s federal ID number. Do not enter a social security number. If you do not have a federal ID number, or if the transfer is of unimproved land for less than $25,000 or land with improvements for less than $50,000, you may enter all 0s in this fi eld. e) through h): Enter the mailing address for the buyer after the purchase of this property.

Line 4. Grantor/Seller. a) & c): Enter one name on each available line, beginning with last name fi rst. If more than two sellers, complete a Supplemental Form. b) & d): If a business entity is entered on a) or c), enter the entity’s federal ID number. Do not enter a social security number If you do not have a federal ID number, or if the transfer is of unimproved land for less than $25,000 or land with improvements for less than $50,000, you may enter all 0s in this fi eld. e) through h): Enter the mailing address for the seller after the purchase of this property.

Line 5. Property. a): Enter the appropriate

don’t know the exact acreage, enter an estimate based on the available information. The acreage recital is for MRS purposes only and it does not constitute a guarantee to the buyer of the acreage being conveyed. EXCEPTION: If the transferred property is a gift, you do not need to complete lines b) and d).

Line 6. Transfer tax. a): Enter the actual sale price or “0” if the transfer

is a gift. b): If you entered 0 or a sale price that is considered nominal on line a), enter the fair market value of the property on this line. The fair market value is based on the estimated price a property will bring in the open market and under prevailing market conditions in a sale between a willing buyer and a willing seller and must reflect the value at the time of the transfer. c): If either party is claiming an exemption from the transfer tax, check this box and enter an explanation of the reason for the claim. See 36 M.R.S. §

Line 7. Date of transfer. Enter the date of the property transfer, which refl ects when the ownership or title to the real property is delivered to the purchaser. This date may not be the same as the recording date.

Line 8. Classified. Check the box if the property is enrolled in one of the current use programs. Current use programs are tree growth, farm and open space, and working waterfront.

Line 9. Special circumstances. If the sale of the property was either substantially more or less than the fair market value, check this box and enter an explanation of the circumstances.

Line 10. Income tax withheld. Nonresident sellers are subject to real estate withholding under 36 M.R.S. §

Line 11. Declaration(s) under penalty of perjury. Please provide the name, mailing address, phone number, and email address of the person or company preparing this form if diff erent from the parties of the transaction.

PROPERTY TYPE CODES

VACANT LAND |

|

COMMERCIAL |

|

INDUSTRIAL |

|

RESIDENTIAL |

|

MISC CODES |

|

Rural |

101 |

Mixed use |

301 |

Gas and oil |

401 |

Rural |

201 |

Government |

501 |

Urban |

102 |

5+ unit apt. |

303 |

Utility |

402 |

Urban |

202 |

Condominium |

502 |

Oceanfront |

103 |

Bank |

304 |

Gravel pit |

403 |

Oceanfront |

203 |

Timeshare unit |

503 |

Lake/pond front |

104 |

Restaurant |

305 |

Lumber/saw mill |

404 |

Lake/pond front |

204 |

Nonprofi t |

504 |

Stream/riverfront |

105 |

Medical |

306 |

Pulp/paper mill |

405 |

Stream/riverfront |

205 |

Mobile home park |

505 |

Agricultural |

106 |

Office |

307 |

Light manufacture |

406 |

Mobile home |

206 |

Airport |

506 |

Commercial zone 107 |

Retail |

308 |

Heavy manufacture |

407 |

207 |

Conservation |

507 |

||

Other |

120 |

Automotive |

309 |

Other |

420 |

Other |

220 |

Current use |

|

|

|

Marina |

310 |

|

|

|

|

classifi cation |

508 |

|

|

Warehouse |

311 |

|

|

|

|

Other |

520 |

|

|

Hotel/motel/inn |

312 |

|

|

|

|

|

|

|

|

Nursing home |

313 |

|

|

|

|

|

|

|

|

Shopping mall |

314 |

|

|

|

|

|

|

|

|

Other |

320 |

|

|

|

|

|

|

| Fact Name | Description |

|---|---|

| Form Usage | The Maine Real Estate Transfer Tax Declaration (Form RETTD) must be filed with the county Registry of Deeds alongside the recording of the accompanying deed. |

| Applicable Tax | A tax of $2.20 for each $500 of property value is collected, shared equally between the purchaser and the seller. |

| Requirement for Supplemental Form | If the property is located in more than one municipality or involves more than two sellers or buyers, a Supplemental Form is required. |

| Transfer Tax Exemptions | Exemptions from the transfer tax can be claimed under certain conditions as specified in 36 M.R.S. § 4641-C. |

| Nonresident Income Withholding | Nonresident sellers may be subject to real estate withholding under 36 M.R.S. § 5250-A, depending on specific criteria. |

| Unique Codes for Property Types | The form requires selection of a property type code best describing the property being sold, with codes provided for various categories like residential, commercial, and industrial. |

Filling out the Maine Real Estate Transfer Tax Declaration (Form RETTD) is an important step in the process of transferring property ownership within the state of Maine. This document must be filed with the county Registry of Deeds when the accompanying deed is recorded, as it helps calculate the tax that needs to be paid based on the property's value. Here’s a simple guide to help you complete the form accurately.

Once all sections are completed, review the form to ensure accuracy and completeness. Remember, this form plays a crucial role in the property transfer process, making it vital to handle it carefully and precisely.

The Maine Real Estate Transfer Tax Declaration Form RETTD is a document required to be filed with the county Registry of Deeds when a deed transferring real estate is recorded. This form helps to calculate the transfer tax due based on the value of the property being transferred.

Both the grantor (seller) and the grantee (buyer) of real estate in Maine are required to complete and file Form RETTD as part of the property transfer process.

The transfer tax in Maine is $2.20 for every $500 of the property's value. This tax is split equally between the buyer and the seller unless otherwise agreed upon.

The purchase price should be entered on the form. If the transfer is a gift or sold for a nominal value, the fair market value should be used instead, reflecting what the property would likely sell for under current market conditions between a willing buyer and seller.

There are various exemptions available for the real estate transfer tax, which include but are not limited to:

If the transferred property spans more than one municipality or consists of multiple parcels, a Supplemental Form must be completed in addition to the main Form RETTD.

Yes, special circumstances that may affect the fair market value, such as the property being sold for significantly more or less than its market value due to certain conditions, should be noted on the form. An explanation of the circumstances should be provided.

For both the grantee (buyer) and the grantor (seller), the following information is needed:

More information and assistance with the Real Estate Transfer Tax Declaration Form RETTD can be found by visiting the official Maine government website at www.maine.gov/revenue/propertytax/transfertax/transfertax.htm or by contacting the Property Tax Division at 207-624-5606.

Filling out the Maine Real Estate Transfer Tax Declaration Form (RETTD) can be complex, and mistakes can lead to issues with your real estate transaction. Here are six common mistakes people make when completing this form:

When filling out the Maine RETTD form, attention to detail is critical. Avoiding these common mistakes will help ensure a smoother real estate transaction and proper tax handling.

When dealing with real estate transactions in Maine, particularly where the Maine Real Estate Transfer Tax Declaration Form (RETTD) is involved, several other forms and documents are frequently used to ensure a transaction's compliance with state laws and regulations. These documents are critical for different aspects of the transfer process, from declaring property value to addressing unique circumstances surrounding the sale.

These forms collectively provide a comprehensive framework for reporting and assessing real estate transactions in Maine. They help to clarify the specifics of each transaction, ensure tax compliance, and support the accurate recording of property transfers in municipal and state records. Therefore, understanding and accurately completing these documents can significantly aid in the smooth execution of real estate transactions.

The Maine Real Estate Transfer Tax Declaration form (Form RETTD) shares similarities with other tax and declaration forms used across various jurisdictions and contexts in the United States. Each form, though tailored for specific transactions or tax requirements, encompasses structured sections for personal and property details, transaction-specific information, exemption claims, and a declaration under penalty of perjury.

One similar document is the Uniform Residential Loan Application used in the mortgage industry. Like the Maine Form RETTD, this application requires detailed information about the borrower (or grantee) and co-borrower, akin to the grantee/purchaser and grantor/seller sections. It includes property information and the financials of the transaction, paralleling the purchase price or fair market value reporting on the tax form. This document also necessitates a declaration or attestation by the applicants about the veracity of the information provided.

The Federal Estate Tax Return (Form 706) resembles the Maine tax form in its requirement for detailed disclosure of the decedent's property and transaction values, similar to the property and transfer tax details. Both documents serve as declarations with legal bindings, wherein the respective preparers must affirm the accuracy and completeness of the information under penalty of perjury.

State-specific Sales and Use Tax forms, which businesses must file, echo the RETTD's structure by necessitating detailed transaction information, seller and buyer details, and property descriptions if relevant. These forms also assess the transaction's tax implications based on the reported values, mirroring the purpose of the transfer tax determination in the Maine document.

The HUD-1 Settlement Statement, used in real estate transactions, shares a core similarity with the Maine Form RETTD in itemizing the financials of a property transfer, though it encompasses a broader range of transactional details and closing costs. Both documents categorize financial responsibilities between the parties involved and provide a comprehensive look at the property exchange's financial outcome.

The Internal Revenue Service's W-9 form, Request for Taxpayer Identification Number and Certification, although fundamentally a tax identification document, parallels the RETTD's sections that require the identification of parties through tax IDs. Such identification enables transparency and accountability in financial transactions, ensuring proper tax reporting and compliance.

Local zoning and land use permit applications can also be considered akin to the RETTD, especially in sections requiring detailed descriptions of the property. These documents often require applicants to describe the property's current and intended use, mirroring the RETTD’s requirement to specify the property type and details about its current classification and use.

The Agricultural Conservation Easement Program (ACEP) application, although more specific in its conservation focus, resembles the RETTD by requiring property descriptions, current use classification, and owner information. Both forms also include declarations by the individuals completing the forms, affirming the truthfulness of the information provided.

Lastly, the Declaration of Homestead forms, available in various states, require homeowners to provide specific property details, ownership information, and, often, the property's value. These forms, much like the Maine tax form, are filed with local government entities and serve as formal declarations with legal implications regarding the property's status and the owner's rights.

When it comes to filling out the Maine Real Estate Transfer Tax Declaration Form (RETTD), accuracy and attention to detail are paramount. Here's a list of dos and don'ts to guide you through the process:

By adhering to these guidelines, individuals can ensure that their Maine Real Estate Transfer Tax Declaration is completed correctly and efficiently, facilitating a smoother transfer process.

When it comes to navigating the intricacies of tax forms, myths and misunderstandings can complicate the process. The Maine Real Estate Transfer Tax Declaration Form (RETTD) is no exception. Here are eight common misconceptions explained to help demystify the process.

By clearing up these misconceptions, individuals involved in the transfer of real estate in Maine can navigate the process with more confidence and accuracy. Remember, when dealing with legal documents and tax forms, understanding the specifics matters greatly.

Filling out and using the Maine Real Estate Transfer Tax Declaration form requires attention to detail and an understanding of specific requirements. Here are key takeaways to guide you through the process:

It's critical to correctly declare the actual sale price or mark it as “0” if the transfer is a gift, providing the fair market value in the latter case. If either the buyer or seller is a nonresident, special attention should be paid to the income tax withholding requirements to ensure compliance. Remember, all declarations made on the form should be under penalty of perjury, indicating that to the best of one's knowledge, the information provided is true, correct, and complete.

Completing the Maine Real Estate Transfer Tax Declaration form accurately is crucial for a lawful transfer of property. Taking the time to review each requirement and seek clarification when needed can help streamline the process for all parties involved.

Maine Rew 5 - Entails a thorough process to document any capital improvements made to the property, which can affect the tax withholding calculation.

Afppgmc Online Updating - An avenue for addressing grievances regarding unpaid pensions, ensuring prior service members or their families can claim their rightful benefits.