Download Maine Rew 5 Template in PDF

Download Maine Rew 5 Template in PDF

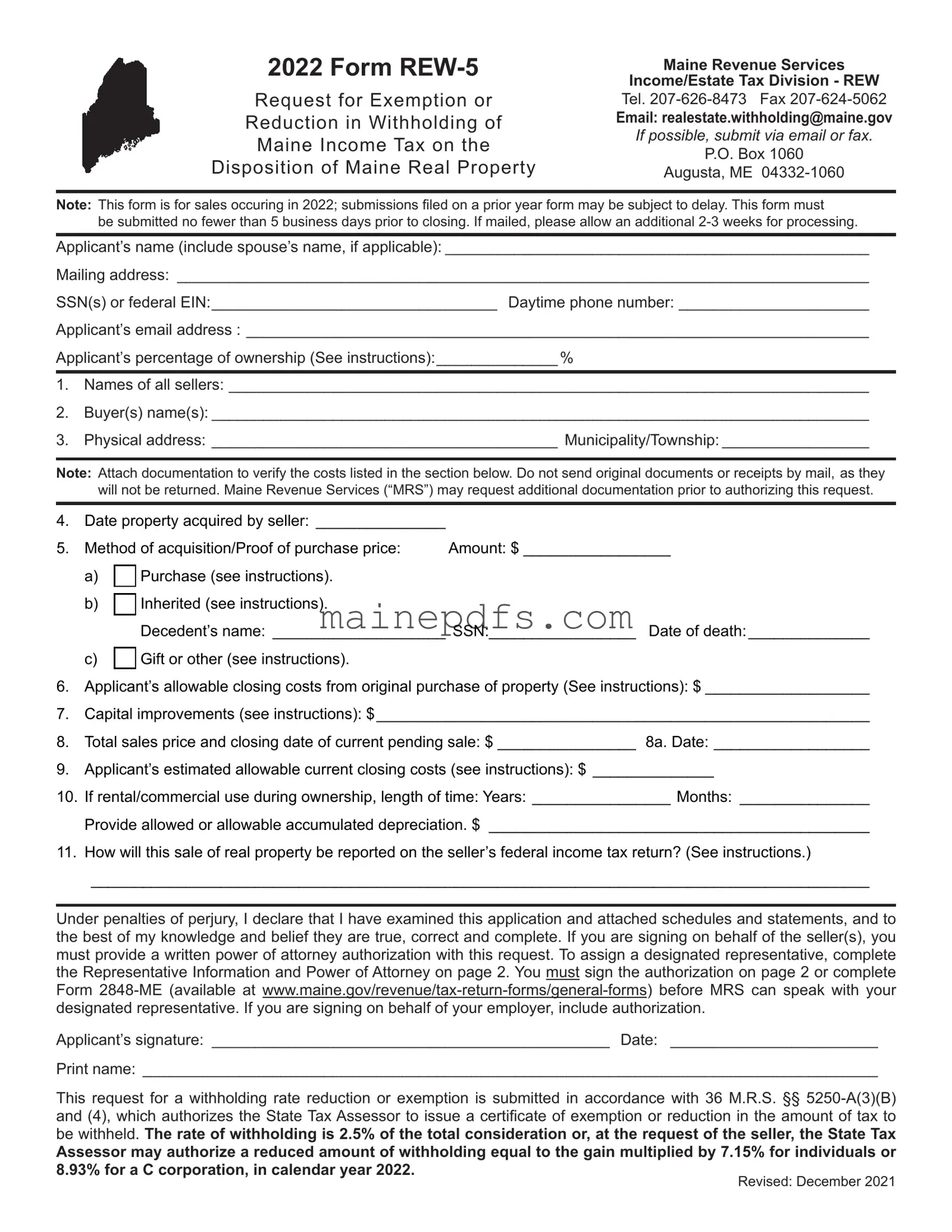

The Maine Form REW-5 is a crucial document for individuals dealing with the disposition of real property in Maine, particularly for nonresidents. Filed with Maine Revenue Services, its primary purpose is to request an exemption or reduction in withholding Maine income tax at the time of a property sale. This provision is guided by stringent requirements, necessitating the submission of the form no later than five business days before the property's closing date. Key details required include the seller's information, a comprehensive list of all involved parties, details of the property, and a transparent account of the financial transactions linked to the acquisition and proposed sale of the property. Additionally, it requires disclosure of any rental or commercial use of the property, estimated closing costs, and specifies how the sale will be reported on the seller's federal income tax return. The form also touches on designating a representative through a Power of Tax, ensuring the seller can have someone authorized to deal with Maine Revenue Services on their behalf. With its comprehensive nature, the form plays a pivotal role in ensuring compliance with Maine's tax laws, potentially mitigating the financial liabilities for sellers by accurately quantifying the tax obligations in line with the actual gains realized from the property transaction.

2022 Form

Request for Exemption or Reduction in Withholding of Maine Income Tax on the Disposition of Maine Real Property

Maine Revenue Services

Income/Estate Tax Division - REW

Tel.

Email: realestate.withholding@maine.gov

If possible, submit via email or fax.

P.O. Box 1060

Augusta, ME

Note: This form is for sales occuring in 2022; submissions filed on a prior year form may be subject to delay. This form must

be submitted no fewer than 5 business days prior to closing. If mailed, please allow an additional

Applicant’s name (include spouse’s name, if applicable): _________________________________________________

Mailing address: ________________________________________________________________________________

SSN(s) or federal EIN:_________________________________ Daytime phone number: ______________________

Applicant’s email address : ________________________________________________________________________

Applicant’s percentage of ownership (See instructions):______________ %

1.Names of all sellers: __________________________________________________________________________

2.Buyer(s) name(s): ____________________________________________________________________________

3.Physical address: ________________________________________ Municipality/Township: _________________

Note: Attach documentation to verify the costs listed in the section below. Do not send original documents or receipts by mail, as they will not be returned. Maine Revenue Services (“MRS”) may request additional documentation prior to authorizing this request.

4. |

Date property acquired by seller: _______________ |

|

||

5. |

Method of acquisition/Proof of purchase price: |

Amount: $ _________________ |

||

|

a) |

|

Purchase (see instructions). |

|

|

|

|

||

|

|

|

|

|

|

b) |

|

Inherited (see instructions). |

|

|

|

|

Decedent’s name: ____________________ SSN:_________________ Date of death:______________ |

|

c)

Gift or other (see instructions).

Gift or other (see instructions).

6.Applicant’s allowable closing costs from original purchase of property (See instructions): $ ___________________

7.Capital improvements (see instructions): $_________________________________________________________

8.Total sales price and closing date of current pending sale: $ ________________ 8a. Date: __________________

9.Applicant’s estimated allowable current closing costs (see instructions): $ ______________

10.If rental/commercial use during ownership, length of time: Years: ________________ Months: _______________

Provide allowed or allowable accumulated depreciation. $ ____________________________________________

11.How will this sale of real property be reported on the seller’s federal income tax return? (See instructions.)

__________________________________________________________________________________________

Under penalties of perjury, I declare that I have examined this application and attached schedules and statements, and to the best of my knowledge and belief they are true, correct and complete. If you are signing on behalf of the seller(s), you must provide a written power of attorney authorization with this request. To assign a designated representative, complete the Representative Information and Power of Attorney on page 2. You must sign the authorization on page 2 or complete Form

Applicant’s signature: ______________________________________________ Date: ________________________

Print name: _____________________________________________________________________________________

This request for a withholding rate reduction or exemption is submitted in accordance with 36 M.R.S. §§

be withheld. The rate of withholding is 2.5% of the total consideration or, at the request of the seller, the State Tax

Assessor may authorize a reduced amount of withholding equal to the gain multiplied by 7.15% for individuals or 8.93% for a C corporation, in calendar year 2022.

Revised: December 2021

Representative Information (complete only if you want someone to represent you during the real estate withholding process)

Representative name (and title, if applicable)

Firm or company name

Mailing address

City, state, zip

Country (if not United States)

Email address

Telephone number

Limited Power of Attorney (complete only if you want someone to represent you during the real estate withholding process)

By signing below, the selling party appoints the individual named in the above section to act as their representative with authority to receive confidential information and to discuss your tax records, related to this form, with MRS. I understand

that my representative may not act on my behalf, unless I provide a Form

Seller signature

Print name (and title, if applicable)

Date

Additional seller signature (if applicable)

Print name (and title, if applicable)

Date

General Instructions

Purpose of Form: To request an exemption or reduction in withholding of Maine income tax on the disposition of Maine real property.

Who may File: A seller (individual, firm, partnership, association, society, club, corporation, estate, trust, business trust, receiver, assignee or any other group or combination acting as a unit) of Maine real property who, at the time of closing, is a nonresident of Maine.

Withholding Certificate Issued by the State Tax Assessor: A withholding certificate may be issued by the

State Tax Assessor to reduce or eliminate withholding on transfers of Maine real property interests by nonresidents.

The certificate may be issued if:

1.No tax is due on the gain from the transfer; or,

2.Reduced withholding is appropriate because the 2.5% amount exceeds the seller’s maximum Maine income tax liability on the gain realized from the sale. The maximum income tax liability is equal to the seller’s capital gain multiplied by 7.15% (8.93% for corporations).

If one of the above is applicable, apply for the certificate no later than five business days prior to closing. Do not apply if

the maximum Maine income tax liability exceeds 2.5% of the consideration.

Foreclosure Sale: If property is subject to foreclosure and the consideration received for the property does not exceed the debt secured by that property, no Maine income tax withholding is required. Foreclosure sale means a sale of real property incident to a foreclosure and includes a mortgagee’s sale of real estate owned property of which the mortgagee, or

of a previous foreclosure auction. MRS does not issue withholding exemption certificates for this type of foreclosure

sale (see Rule 803 and 36 M.R.S. §

2

Specific Instructions

Email Form

Applicant’s name: Enter the applicant’s (seller’s) name.

NOTE: If there are multiple sellers of the property, each

applicant (seller) must complete a separate Form REW-

5, except that married taxpayers that will file a joint Maine individual income tax return requesting a withholding exemption or reduction may complete one form, listing both names and SSN’s on the form.

Mailing address: Enter the applicant’s current mailing address.

Social Security Number (SSN) or Employer Identification

Number (EIN): Enter the SSN or EIN of the applicant listed on this form. If applicable, enter your spouse’s SSN.

Line 1. If applicant’s ownership percentage is less than 100%, all sellers must be listed on this line. The seller(s) are typically listed on the Purchase and Sale Agreement. Attach additional pages, if necessary.

Line 2. Enter the names(s) of the buyer(s). The buyers are typically listed on the Purchase and Sale Agreement. Attach additional pages, if necessary.

Line 3. Enter the physical address of the property being sold.

Line 4. Enter the date the seller acquired the property.

Line 5. Indicate the method by which the seller obtained ownership of the property.

a)If you purchased the property, attach verification of the original sales price, such as

b)If you inherited the property, provide a complete appraisal dated within six months of the decedent’s death or a copy of the tax assessment from the town. Enter the decedent’s name, SSN and the date of death in the spaces provided.

c)If you received the property as a gift, provide documents to verify the original purchase price paid by the previous owner. If you cannot locate these documents, the town where the property is located may have a record of the purchase price. As a general rule, for purposes of determining the gain, you will use the donor’s adjusted basis at the time of gift as your basis.

Line 6. Enter the amount of the allowable original closing costs you paid at the time of acquisition*. Also see line 9.

Line 7. Provide a list of capital improvements made to the home along with the cost of each improvement. Do

not include repairs made to the property. For example:

Cleaning or fixing a furnace is not a capital improvement, but installing a new furnace is. If you built the home, provide the information for the build. You can make a detailed list of the items purchased (including the cost of each and providing

receipts), provide a copy of the contract with the builder, provide the building permit filed with the town, or provide the tax assessment from the year you received the certification

of occupancy. Attach additional pages as needed.

Line 8. Enter the total gross sales price of the property. Do not subtract any fees. The sale price should match the sales price on the Purchase and Sales Agreement. If there are multiple sellers, list this seller’s ownership percentage.

Line 8a. Enter the closing date for the sale of this property.

Line 9. Enter the amount of the applicant’s allowable closing costs from the current sale of this property*. Also see line 6.

*Certain closing costs do not qualify. If available, enclose a copy of the

For more information about selling your home, determining basis, reporting the sale, capital improvements and costs, see IRS Publication 523.

Line 10. If the property was rented or used commercially, enter the allowed, or allowable, accumulated depreciation determined in accordance with the Internal Revenue Code.

Line 11. Indicate whether the sale will be reported as a gain, loss, exclusion, installment sale or

Representative Information & Limited Power of Attorney

Although not required, you may designate someone to represent you during the real estate withholding process. To do so, complete the Representative Information and Limited Power of Attorney sections on page 2 of Form

designated representative must be an individual, although a firm cannot be designated as your representative, an individual of a firm can be.

Appointing a Limited Power of Attorney designates a representative to receive confidential information and to discuss tax records related to your Form

with MRS. The designated representative may not act on your behalf, unless a completed Form

3

| Fact Number | Fact Detail |

|---|---|

| 1 | The Form REW-5 is a request for exemption or reduction in withholding of Maine income tax on the disposition of Maine real property. |

| 2 | This form is applicable to individuals, firms, partnerships, and other entities disposing of real property in Maine who are nonresidents at the time of closing. |

| 3 | Applicants should submit the Form REW-5 no less than five business days before the closing date. If mailed, an additional 2-3 weeks should be allowed for processing. |

| 4 | The governing law for this process is 36 M.R.S. §§ 5250-A(3)(B) & (4), which allows the State Tax Assessor to issue a certificate for no tax due or a reduced withholding amount. |

| 5 | The standard withholding rate is 2.5% of the total consideration or, at the request of the seller, a reduced amount based on the gain multiplied by applicable percentages for different types of entities. |

| 6 | Submission of this form and all supporting documents can be made via email to realestate.withholding@maine.gov or faxed to (207) 624-5062 for faster processing. |

Filling out the Maine REW-5 form is an important step for those looking to request an exemption or reduction in the withholding of Maine income tax after the sale of real property. Its completion is crucial for ensuring that sellers provide all necessary information to Maine Revenue Services (MRS) for proper processing. Here's a straightforward, step-by-step guide to help you accurately complete the form.

After completing the form, submit it along with any supporting documents to Maine Revenue Services, preferably via email or fax for faster processing. Remember to submit the form at least five business days before the closing date to allow MRS adequate time for review. If mailing, anticipate an additional two to three weeks for processing. Taking these steps ensures that your request for exemption or reduction in real estate tax withholding is properly considered.

Form REW-5 is a request form for either an exemption from or a reduction in the withholding of Maine income tax when selling real property in Maine. It is specifically for transactions involving the transfer of real estate by nonresident sellers.

Nonresident individuals, firms, partnerships, associations, corporations, estates, trusts, or other entities selling real estate in Maine should file Form REW-5 if they seek to reduce or eliminate the standard withholding tax rate on the sale’s proceeds.

This form must be submitted to Maine Revenue Services no fewer than five business days before the closing date of the property sale. If mailed, additional processing time of 2-3 weeks should be allowed.

Maine Revenue Services may request various documents to support the request for a withholding exemption or reduction, such as evidence of the original purchase price, appraisals, proof of capital improvements, closing statements, and, if applicable, documentation relating to rental or commercial use of the property.

Yes, you can submit Form REW-5 and all supporting documents either via email to realestate.withholding@maine.gov or by fax to (207) 624-5062. Electronic submission is encouraged for faster processing.

If the ownership percentage is less than 100%, you need to list all sellers involved in the transaction. Similarly, all buyers should be listed as they appear on the Purchase and Sale Agreement. If there is insufficient space on the form, attach additional pages with the required information.

If you're unsure whether the sale of the property will result in a financial gain or loss, leave the relevant section (line 11) on Form REW-5 blank. Consultation with a tax professional can help clarify this before you file.

Filling out forms for any tax-related process can be a bit tricky, and the Maine Form REW-5, which is used to request an exemption or a reduction in withholding on the sale of Maine real property, is no exception. Accuracy and attention to detail are paramount because mistakes can cause delays or affect the withholding amount. Here are seven common mistakes people make when filling out this form:

Overall, when completing the Maine REW-5 form, paying close attention to detail, correctly attaching required documents, and double-checking all entered information can help avoid these common mistakes. This will smooth out the process and ensure that your request for an exemption or reduction in real estate withholding is processed efficiently and accurately.

When dealing with the disposition of Maine real property, particularly for nonresidents, the Maine REW-5 form is an essential document. However, this form often does not stand alone in the transaction process. Other documents play crucial roles, ensuring compliance with the law and smoothing the pathway to a successful real estate transaction. Here is a description of various forms and documents that are commonly used alongside the Maine REW-5 form.

Each of these documents serves a specific purpose, contributing to the thorough and compliant execution of a real estate transaction involving nonresident sellers in Maine. Sellers and their representatives should ensure they understand the function and requirements of each document to facilitate a smooth process.

The Federal Form 1099-S, used for reporting the sale or exchange of real estate, shares some common ground with the Maine REW-5 form in terms of purpose. Both documents are closely related to real estate transactions, although the 1099-S is more broadly used to report transactions to the IRS, including sales proceeds, while the REW-5 specifically requests a reduction or exemption in state tax withholding. The key similarity lies in their role in documenting and detailing transactions of property to ensure tax compliance, yet they serve different tax authorities and purposes.

Another document akin to the REW-5 form is the HUD-1 Settlement Statement, which was widely used in real estate transactions to itemize services and fees charged to the borrower by the loan lender before its replacement by the Closing Disclosure form. The HUD-1 and the Maine REW-5 form both play pivotal roles at the closing of real estate transactions, with the HUD-1 providing a detailed list of closing costs and the REW-5 potentially reducing withholding taxes. They support the financial aspects of property transactions, ensuring parties are aware of the costs and taxes due.

The IRS Form 8288, "U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests," is a federal equivalent in the realm of foreign transactions. It's utilized when foreign sellers dispose of U.S. property interests, ensuring tax withholding is correctly managed. Like the Maine REW-5 form, it's fundamentally about withholding taxes on real estate transactions, but the IRS Form 8288 specifically focuses on foreign participants, highlighting how tax obligations change across domestic and international transactions.

Maine's Real Estate Transfer Tax Declaration form, another document in the family of property transaction papers, is also used in the process of selling property within the state. While this form calculates the transfer tax due to the state based on the property's sale price, the REW-5 form addresses income tax withholding on the sale for non-residents. Both forms are critical for legal and tax compliance in real estate sales, ensuring correct taxes are documented and paid to the state.

Lastly, the IRS Form 2848, "Power of Attorney and Declaration of Representative," relates to the REW-5 document in that it allows the designation of a representative to handle tax matters. The REW-5 form includes sections for appointing a representative during the real estate withholding process, similar to how Form 2848 permits individuals to authorize another person to discuss and handle their tax matters with the IRS. Both forms provide a method for taxpayers to ensure their tax-related issues are managed appropriately by granting authority to a trusted representative.

When dealing with the Maine Real Estate Withholding (REW-5) form, careful attention to detail can make the process smoother and help avoid unnecessary delays. Here are five things you should and shouldn't do when completing this form:

Do:

Don't:

When dealing with the Maine REW-5 form, which is utilized for requesting exemptions or reductions in withholding Maine income tax on the sale of real property, various misconceptions can arise. Understanding these misconceptions ensures correct form submission and compliance with state tax laws.

Actually, the REW-5 form is specifically designed for nonresidents or part-time residents selling property in Maine, aiming to reduce or eliminate the withholding on the sale's gains.

In reality, if the sale does not result in a gain, or if the 2.5% withholding exceeds the seller’s maximum tax liability, an exemption or reduction may be applied for using this form.

The correct procedure requires submitting the form at least five business days before closing to ensure processing time.

Maine Revenue Services may request additional documentation and has the discretion to deny the request based on the provided information.

Although submissions through mail are possible, submitting the form via email or fax is encouraged for faster processing.

Each seller must complete an individual form unless they are married and filing a joint return, which allows for a single form submission.

While capital gains are a key component, the form also requires detailed information about acquisition methods, improvements, and use of the property to accurately assess tax obligations.

This section is optional and only necessary if the seller wishes to designate someone else to handle their affairs regarding the real estate withholding process.

Clearing up these misconceptions ensures that potential sellers are better informed about their tax liabilities and obligations, leading to smoother transactions and compliance with the Maine tax code.

Understanding the intricacies of the Maine REW-5 form is essential for those looking to navigate the complexities of real estate transactions involving the disposition of Maine real property. The form plays a critical role in managing tax obligations related to these transactions. Here are six key takeaways about filling out and utilizing the Maine REW-5 form effectively:

Thoroughly completing and submitting the Maine REW-5 form with accurate and comprehensive information can significantly streamline the process of requesting tax withholding exemptions or reductions. This not only aids in ensuring compliance with state tax regulations but also in potentially reducing the financial burden on the seller during the property transfer process.

Registry of Motor Vehicles Maine - Important considerations when determining if you should apply for a seat belt exemption.

Motor Vehicle Maine - This application serves as a gateway for securing temporary permits essential for compliant commercial vehicle operation in Maine.